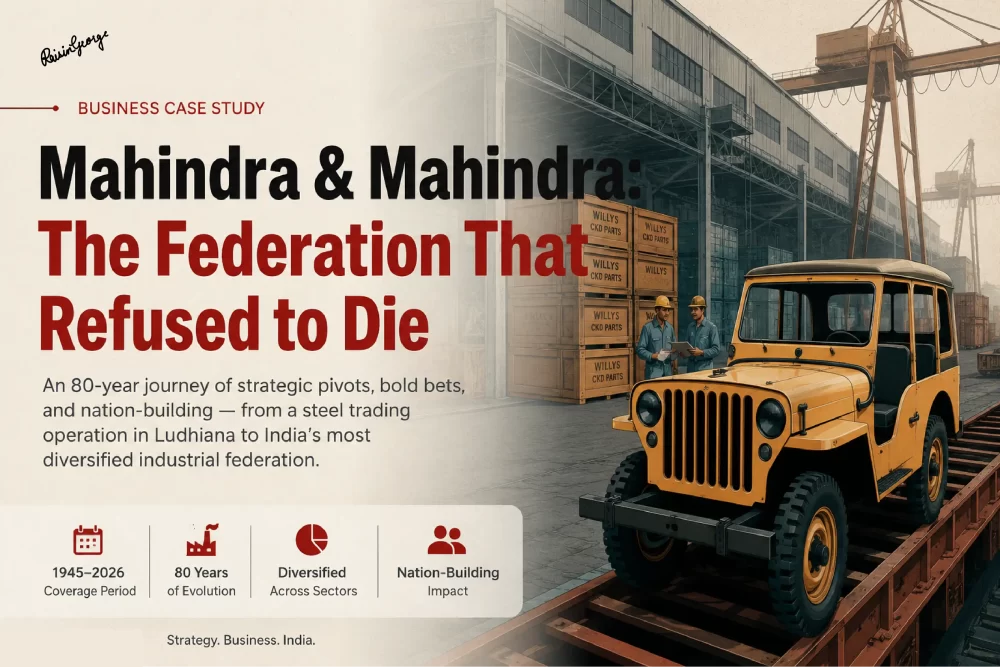

On 2 October 1945, three men filed papers for a steel trading company in Ludhiana, Punjab. Within two years, one of those partners had left for Pakistan — where he went on to become the country's first Finance Minister. The brothers left behind could not afford to reprint their letterheads. So the name stayed.

That name — Mahindra & Mahindra — is today worth tens of billions of dollars in brand equity. It covers tractors sold in Iowa farmlands, armoured vehicles protecting the Indian Army, enterprise software written for British Telecom's back office, and electric SUVs with a claimed range of 683 kilometres backed by Singapore's sovereign wealth fund. The company that survived Partition on a budget constraint now holds a Guinness World Record, runs India's most institutionally governed industrial group, and in FY26 achieved 20.8 percent ROE — higher than its own publicly stated target.

This is not a company that followed a plan. It is one that survived long enough — and failed loudly enough — to discover what it was actually built for.

The full 70-page case study — covering all seven business verticals, the INGLO EV deep-dive, Capital Allocation 2.0, the complete failed ventures audit, and M&M's ownership structure — is available as a free PDF download at the end of this article.

Origin1. The Company Name Was an Accident of Partition

Mahindra & Mohammed was registered on 2 October 1945 in Ludhiana by J.C. Mahindra, K.C. Mahindra, and Malik Ghulam Mohammed. The logic was prosaic: post-war India needed steel and industrial goods, and J.C. Mahindra's government contacts made trading viable. The company's ambitions were modest. The founding circumstances were not.

When Partition arrived in 1947, Malik Ghulam Mohammed departed for Pakistan. He became the country's first Finance Minister and subsequently its Governor-General from 1951 to 1955. The Mahindra brothers were left with letterheads reading "M&M" and a practical decision to make. Reprinting all company stationery was too expensive for the young firm. Since there were two Mahindras in the business, the name became Mahindra & Mahindra — preserved not by brand strategy but by a budget constraint.

The founding philosophy: J.C. Mahindra had studied at Harvard Business School before independence — unusually sophisticated for a colonial-era Indian entrepreneur. The founding approach, as later articulated, was to build capabilities and wait for India to need them. In retrospect, eighty years of company history is a confirmation that this patience was the actual competitive strategy. A brand worth tens of billions of dollars today owed its survival in week one to the cost of ink and paper.

2. The World's Number One Tractor Brand Nobody Talks About

Ask most people which company sells the most tractors in the world and the answer will be John Deere. The correct answer is Mahindra. M&M holds a Guinness World Record for the highest cumulative tractor sales by a single brand in history — four million units by 2024. John Deere, CNH, and AGCO have not matched it by volume, driven entirely by India's unique agricultural structure: hundreds of millions of small-acreage farms, each requiring a sub-50 horsepower machine, creating a sustained volume market no other country replicates at comparable scale.

The strategic origin was a moment of channel intelligence. When M&M entered tractors in 1961 through a joint venture with International Harvester, it already had a rural dealer network built from Willys Jeep distribution that reached villages no competitor had penetrated. It did not need to build distribution for a new product. It simply sold a second product through the same infrastructure.

The farm equipment business is M&M's least publicised vertical and its most structurally profitable. PBIT margins consistently run at 18 to 19 percent — roughly double the automotive segment. A 43 percent domestic market share gives M&M dealer pricing power competitors cannot replicate quickly. The aftermarket parts business compounds this advantage: once a farmer owns a Mahindra tractor, every service, every spare part, every next purchase is weighted back toward the same brand. The 900-plus dealer network with 24-hour service coverage across every Indian district represents sixty years of accumulated capital that no entrant can substitute with advertising spend.

The Swaraj acquisition: When M&M bought Swaraj Tractors of Punjab in 1994, the corporate instinct would have been to rebrand under the Mahindra name. M&M did the opposite. Market data showed Swaraj commanded deeper farmer loyalty in Punjab and Haryana than Mahindra — the name carried regional pride and agricultural heritage. The Swaraj brand was retained. In 2026, it still runs its own production line. Market intelligence overrode corporate ego. This kind of discipline is rarer than it sounds.

3. The ₹600 Crore Bet That Rebuilt an Identity

In the late 1990s, Mahindra was a manufacturer of utility vehicles that urban India did not buy. The Bolero sold to government departments. Jeep derivatives served rural buyers and government agencies. The company needed something that could change how India thought of it — not as a utility manufacturer but as a product company.

Pawan Goenka — who had joined M&M from General Motors' R&D division in Detroit in 1992 — pushed for something that had not been done before in India: build a new vehicle entirely from scratch, with no Willys lineage, no foreign platform, no licensed European or American engine. India's own SUV, designed by Indian engineers.

| Scorpio Project Parameter | M&M Approach | Typical Global OEM Equivalent |

|---|---|---|

| Development cost | ₹550–600 crore | 5x to 8x this figure |

| Engineering team | 120 engineers, average age 27 | 1,000+ specialists across divisions |

| Development timeline | 5 years — concept to showroom | 5–7 years with significantly more capital |

| Platform philosophy | System supplier model — suppliers designed full subsystems to M&M's performance specs | OEM-defined component specifications throughout |

| Launch price | ₹5.99 lakh (June 2002) | No comparable domestic indigenous SUV existed |

| Engine origin | Direct descendant of M&M tractor powertrain | Specialist automotive engine from a global supplier |

The Scorpio's most underappreciated feature was not its design but its engine heritage. The diesel powertrain descended directly from M&M's tractor lineage — a deliberate engineering choice that gave the vehicle a competitive advantage no licensed car could replicate. A rural mechanic who had spent years servicing Mahindra tractors already understood the engine architecture. No specialist tools. No dealer service visit required. In a country where the majority of vehicle breakdowns occur more than 20 kilometres from a service centre, repairability by a local mechanic was not a convenience feature. It was a market penetration strategy embedded in the product.

"The Scorpio proved that M&M could design world-class products indigenously. It gave the company confidence for every subsequent product: the Thar relaunch, the XUV700, and ultimately the Born Electric SUVs."

— Anand MahindraThe Scorpio Classic — the original 2002 model, now in an evolved form — still had an active production line in 2026. The Scorpio-N crossed 100,000 production units since its 2022 relaunch. A vehicle conceived over twenty years ago remains in active market. That is brand durability of a kind very few Indian products have achieved.

Strategic Failure4. SsangYong: The Decade-Long Mistake That Rewrote the Rules

In 2010, M&M paid $463.6 million for a 70 percent stake in SsangYong Motor Company — South Korea's fifth-largest automaker, already through one bankruptcy, with a recent history of a 77-day labour strike during which workers burned parts of their own factory. The stated rationale was valid: technology access for SUV platforms, a global distribution footprint across Europe and Australia, and a path toward becoming a top-10 global automaker by volume. Every part of this logic was reasonable at entry. Every part was wrong in practice.

M&M acquires 70% of SsangYong for $463.6 million. Reverses previous management's layoffs, rehires workers. Humane. Expensive. Sets a tone the organisation could not sustain.

Alturas G4 and Rexton fail to gain traction in India. SsangYong struggles globally against Hyundai, Kia, and Toyota with weaker products, smaller scale, and inferior brand recognition. First clear signals that the thesis is not working.

Consecutive loss years: 2017, 2018, and a ₩341 billion loss in 2019. Analyst consensus hardens: exit. M&M continues capital support. The sunk-cost reasoning begins to take hold.

SsangYong files for bankruptcy. M&M takes a ₹530 crore impairment charge — its biggest quarterly loss in 19 years. COVID accelerated what fundamental product weakness had made inevitable.

SsangYong sold to KG Group. M&M receives effectively nothing meaningful from the sale. Total capital destroyed across 12 years: estimated $600 million to $1 billion, including acquisition, capital infusions, and impairment charges.

The failure had four distinct causes. SsangYong's products were not competitive in their own home market against Hyundai and Kia — only the Tivoli sold well domestically. M&M's frugal engineering culture, supplier development discipline, and distribution methodology did not transfer to a Korean industrial context with different union work structures and cost bases. Cultural DNA is not exportable through an acquisition cheque. The global markets M&M had expected to access — Europe, Australia — required brand investments that SsangYong's product quality could not support. And the exit, when everyone could see it was necessary by 2017 or 2018, was delayed three to four years by the emotional investment in the global automotive brand story.

Why this failure matters more than the capital destroyed: The SsangYong experience became the foundational lesson for Capital Allocation 2.0. When Anish Shah exited 15 businesses in 18 months after April 2021, each exit was the SsangYong lesson applied in advance. The cost of not learning it earlier was somewhere between $600 million and $1 billion. The cost of learning it was that every subsequent capital allocation decision became faster, cleaner, and publicly accountable.

5. The Federation That Is Not a Conglomerate

Anand Mahindra has a specific word for what M&M is: a federation. The distinction matters more than it appears on the surface.

A traditional conglomerate typically features centralised capital allocation, where the parent decides where money flows and subsidiaries compete internally for resources. A federation operates on a fundamentally different logic: each business unit runs with its own CEO, its own profit and loss account, its own board, and — critically — access to external capital without requiring parent approval for every transaction. Tech Mahindra, Mahindra Finance, Mahindra Logistics, and Mahindra Lifespaces are all separately listed entities that attract institutional investors independently of the parent. They stand on their own financial merit in public markets.

| Dimension | Traditional Conglomerate | M&M Federation Model |

|---|---|---|

| Capital access | Parent allocates to subsidiaries | Subsidiaries raise external capital independently |

| Leadership accountability | Subsidiary CEO answers to parent board | Subsidiary CEO accountable to own board plus parent ROE threshold |

| Cross-subsidisation | Common practice in downturns | Prohibited under Capital Allocation 2.0 — exit instead of subsidy |

| Investor visibility | Consolidated P&L obscures segment performance | Separately listed subsidiaries allow segment-specific capital pricing |

| Exit discipline | Rare — emotional attachment to portfolio businesses | Formal: 18% ROE threshold or defined-timeline exit |

The federation works — when it works — because of a single non-negotiable governance mechanism: the 18 percent Return on Equity threshold. Every business must demonstrate a credible path to 18 percent ROE within a defined timeframe. Those that cannot are exited, not subsidised, not indefinitely restructured, not absorbed into a larger division to obscure the underperformance. The valuation challenge that accompanies the model is real: M&M's consolidated market capitalisation persistently trades at a 15 to 25 percent discount to its sum-of-parts valuation. Investors price in the risk of cross-subsidisation. Capital Allocation 2.0 is the specific mechanism designed to close that gap.

Capital Discipline6. Capital Allocation 2.0: The 18% ROE Threshold That Changed Everything

When Anish Shah became M&M's Group CEO and Managing Director in April 2021 — the first non-family MD and CEO in the company's 79-year history — he inherited a specific and well-understood problem. M&M had been the top-performing stock on the NIFTY 50 from 2002 to August 2018, delivering a 31 percent CAGR over that period. From 2018 to 2021, it had significantly underperformed the benchmark. The diagnosis was clear: capital had been deployed in businesses that could not earn their cost of capital.

The IIT Bombay, IIM Ahmedabad, and Wharton alumnus who had spent 14 years at GE Capital installed a framework that was deliberately simple and publicly committed to: every business in the M&M group must demonstrate a credible path to 18 percent Return on Equity within a defined timeframe. Businesses that cannot do so are exited. No exceptions. No indefinite restructuring cycles. No waiting for macro conditions to improve.

How the EV bet was de-risked within Capital Allocation 2.0: The framework did not mean only cuts. When M&M committed $1.5 billion to its EV arm (MEAL), it structured the investment through external capital partners — Temasek and British International Investment — rather than funding the entire buildout from internal accruals. The EV subsidiary could access dedicated capital without straining the parent's returns. Capital Allocation 2.0 governed not just exits but how new business units were capitalised at entry. No bet that threatens the parent's ROE threshold goes unfunded; every bet is funded in a way that does not compromise it.

7. The Monsoon Risk Is Two Simultaneous Risks Arriving Through Two P&L Lines

Most analyst coverage of M&M describes monsoon dependency as a single risk: a deficient monsoon reduces farm income, suppresses tractor demand, and causes a 10 to 15 percent volume decline in the farm equipment segment within a quarter. This framing is incomplete. It misses what is actually happening at a portfolio level.

A deficient monsoon does not arrive through one P&L line. It arrives through two, simultaneously. The same macro shock that defers a farmer's tractor purchase (hitting Vertical 2: Farm Equipment revenues) also triggers elevated non-performing assets in Mahindra Finance's loan book, as farmers who already hold vehicle or tractor loans miss EMI payments due to compressed farm income (hitting Vertical 3: Financial Services provisioning). These are not independent events. They are the same underlying event — a failed harvest — arriving through different accounting entries in the same reporting quarter.

The compounding mechanism: When rainfall fails, a farmer expecting a specific harvest income finds both his cash flow and his confidence impaired. He delays the tractor purchase (tractor segment volume falls). The same farmer, already holding a Mahindra Finance loan on an existing tractor or vehicle, misses an EMI (Mahindra Finance Stage 3 NPAs rise, requiring provisioning). M&M's consolidated balance sheet absorbs both effects simultaneously from the same root cause. This is a portfolio concentration risk, not a single-vertical risk — and it is structurally more serious than most monsoon-risk disclosures convey.

M&M's partial mitigant is international tractor diversification. M&M is the number one sub-50 HP tractor brand in the United States, serving hobby farmers and small-acreage operators, with growing presence in Africa and Australia. But these markets represent less than 30 percent of farm segment revenue today. Building sufficient international volume to meaningfully offset an Indian monsoon failure is a decade-long project. In the near term, a deficient monsoon remains a portfolio concentration event, not a single-segment risk — and it is worth modelling accordingly.

EV Strategy8. INGLO: A Purpose-Built EV Platform With Sovereign Wealth Fund Backing

M&M's previous electric vehicles — including the Mahindra Reva and the XUV400 — were ICE conversions: existing petrol or diesel platforms adapted to carry a battery pack. The engineering compromises were inherent. INGLO, announced in 2022, was built on a different premise entirely. It is a ground-up electric skateboard architecture in which the flat battery floor is the structural foundation of the vehicle. No transmission tunnel. No driveshaft intrusion. The entire geometry is optimised for battery geometry from first principles — not retrofitted around an engine that was never there.

| INGLO Platform Specification | Detail |

|---|---|

| Battery pack options | 59 kWh or 79 kWh — same physical footprint, enabling trim variants without platform changes |

| Peak charging rate | 175 kW — 80% charge in under 30 minutes |

| Claimed range | 542 km to 683 km depending on variant and battery configuration |

| Drive configurations | RWD and AWD (dual-motor) — targets performance and family buyers separately |

| Software platform | MAIA — M&M's proprietary automotive computing platform with OTA updates and remote diagnostics |

| IP ownership | Fully indigenous — zero royalties, no licensor ceiling on development velocity |

| EV arm structure | MEAL (Mahindra Electric Automobile Ltd) — separate subsidiary with external equity partners |

The capital structure of the INGLO programme is structurally unusual in the global EV landscape. Rather than funding M&M's EV arm entirely from internal accruals — which would have strained the parent's ROE metrics during the buildout period — M&M brought in Temasek (Singapore's sovereign wealth fund, with over $380 billion in assets under management) and British International Investment (the UK's development finance institution) as equity partners in MEAL. Two government-backed investors taking equity in what is effectively a conglomerate's internal EV startup provides balance sheet de-risking, international credibility, and governance accountability simultaneously. It is the anchor client model applied to capital formation.

MEAL reached EBITDA-positive status by Q4 FY25 — a milestone most global EV ventures do not hit until they are past 100,000 annual units of scale. The EV roadmap to 2030 includes six additional models. The Electric Thar is strategically the most important of them: it reframes the EV narrative from urban commuter appliance to off-road adventure machine. This addresses the single most significant psychological barrier to EV adoption among M&M's rural and semi-urban customer base — the perception that electric vehicles are city products for city people. If a Thar can ford a river on electricity, the objection dissolves.

Brand & Leadership9. Three Generations of Harvard — and a Zero-Cost Marketing Engine With 11 Million Followers

J.C. Mahindra, the company's founder, was among Harvard Business School's earliest Indian graduates — a remarkable distinction for a student from colonial India in the early twentieth century. His grandson Anand Mahindra attended Harvard College before HBS, and today sits on HBS's Board of Overseers, the institution's highest governing body. Three generations. One institution. A thread of intellectual aspiration running through the company's DNA that gave successive M&M leaders successive exposures to global management thinking and the institutional networks that accelerated early American business partnerships and the international investor relationships that followed.

The X strategy and what it actually is: Anand Mahindra's personal account on X (formerly Twitter) has accumulated 11 million-plus followers — a reach that exceeds most Indian automotive advertising campaigns, at zero media cost to M&M. His content approach is deliberate: amplifying user-generated videos of Thar river-fording, XUV700 crash-survivor stories, off-road adventure footage. He responds publicly to customer complaints. He positions the chairman as accountable in real time, on a public platform. A Thar waterfall video reaching 11 million people carries more purchase intent than a high-budget television campaign because the audience perceives it as unscripted and authentic. This is brand strategy disguised as personality — and it is effective precisely because the disguise is good.

The governance dimension of the M&M leadership story is as significant as the marketing one. When Anand Mahindra transitioned to Non-Executive Chairman in November 2021, he was not retiring — he was making a deliberate governance move. By stepping back from operational decisions, he gave Anish Shah the room to build his own leadership identity without the founding family's presence hovering over day-to-day choices. The transition was publicly announced five months before Shah's start date. Shah was progressively elevated through four roles — Group Strategy Head, President and CEO for New Businesses, Deputy MD, then MD and CEO — building credibility at each level before assuming full authority. In a country where most family-controlled conglomerates treat succession as the event that happens when the patriarch stops showing up, M&M's structured transition is a case study in how to transfer control without losing institutional momentum.

Ownership & Governance10. Institutions Own M&M, Not the Family — and That Is the Governance Point

The Mahindra family holds approximately 18 to 19 percent of their own conglomerate. This is remarkably low for a founding-family Indian business. Tata Sons holds a higher effective stake through its trust structure. Most Birla companies carry significantly higher promoter ownership. At M&M, Foreign Portfolio Investors hold 38.5 percent and Domestic Institutional Investors — mutual funds, LIC, insurance companies — hold a further 26 percent. Institutions collectively control the company more than the founding family does.

This ownership structure carries a governance consequence that matters more than the raw percentages. The Mahindra family cannot ignore institutional shareholder pressure the way a 60 to 70 percent promoter-held conglomerate can. Capital Allocation 2.0 was not purely philosophical. It was the rational response of a management team that understood its institutional shareholder base had both the voting power and the analytical sophistication to demand accountability — and had been pricing in the conglomerate discount for years as an expression of that demand.

The discount and its partial closing: M&M's consolidated market cap persistently trades at a 15 to 25 percent discount to its sum-of-parts valuation. Auto, Farm Equipment, Tech Mahindra, and Mahindra Finance each trade on different multiples. Investors apply a holding company penalty because they price in the risk that profitable business cash flows will be used to rescue struggling subsidiaries. The 15-exit sprint and the 18% ROE threshold are the specific mechanisms designed to close this gap. The discount has narrowed since 2021. It will close fully only through sustained multi-year ROE delivery across all arms simultaneously — which is exactly what Anish Shah's quarterly public updates are designed to demonstrate.

Ten Facts About Mahindra & Mahindra That Rarely Appear in Analyst Reports

Malik Ghulam Mohammed — one of M&M's two founding partners alongside J.C. Mahindra — left at Partition in 1947 and became Pakistan's first Finance Minister, then its Governor-General from 1951 to 1955. M&M was founded by men who went on to shape two nations.

After Partition, with their founding partner departed, the Mahindra brothers kept the M&M letterhead because reprinting all company stationery was financially prohibitive. One of the world's most valuable corporate brands was preserved by a budget constraint in 1947.

The Scorpio's diesel engine descended directly from M&M's tractor powertrain — by design. A mechanic who serviced Mahindra tractors already understood the architecture. In a country where most vehicle breakdowns occur far from service centres, repairability was a product feature, not a convenience.

M&M holds the Guinness World Record for the highest cumulative tractor sales by a single brand — 4 million units by 2024, ahead of John Deere and CNH by volume. India's small-farm agricultural structure created a sustained volume market no other country replicates at comparable scale.

J.C. Mahindra (founder) was among HBS's earliest Indian graduates. Anand Mahindra attended Harvard College then HBS, and today sits on HBS's Board of Overseers — the school's highest governing body. Three generations, one institution, an unbroken thread of global management exposure.

The Thar's body style traces directly to the 1949 Willys CJ-5 Jeep — the first vehicle M&M ever assembled and sold. The current Thar 4-door is simultaneously a globally benchmarked off-road SUV and a direct bloodline descendant of a 75-year-old American working vehicle. Few automotive lineages claim uninterrupted continuity across three-quarters of a century.

Temasek — Singapore's sovereign wealth fund with $380B+ AUM — and British International Investment, the UK's development finance institution, have taken equity stakes in MEAL, M&M's Born Electric arm. Two government-backed institutions as equity partners in an internal startup is structurally unusual and deliberately strategic.

M&M was ranked #44 in TIME Magazine's World's Best Companies — the only Indian company in the global Top 100 at time of ranking, ahead of hundreds of larger Western multinationals across employee satisfaction, revenue growth, and sustainability metrics.

The Armado light strike vehicle is the first armoured tactical vehicle designed by India's private sector with full IP ownership. Every previous Indian Army vehicle was built on a licensed or foreign-designed platform. M&M owns the Armado's design, IP, and manufacturing capability — and can export without licensor approval.

When M&M acquired Swaraj Tractors in 1994, the corporate playbook would have called for rebranding under Mahindra. Market data showed Punjabi farmers had deeper loyalty to Swaraj than Mahindra. M&M kept the name. In 2026, Swaraj still runs its own production line. Data overrode instinct. That is rarer than it sounds.

The Failed Ventures Audit: Six Mistakes and What Each One Taught

| Venture | Period | Severity | The Lesson |

|---|---|---|---|

| SsangYong Motor | 2011–2022 | Critical | Cultural DNA does not transfer via acquisition cheque. Exit triggers must be defined at entry, not at deterioration. Total capital destroyed: est. $600M–$1B. |

| Mahindra Renault JV / Logan | 2005–2010 | Significant | Indian mass-market buyers rejected a boxy European design. Renault's cost structure misaligned with Indian volume economics. Entry thesis was valid; execution assumptions were European. |

| US Pickup Truck (Global Vehicles USA) | 2008–2012 | Significant | Underestimated US dealer relationship complexity. Product required fundamental redesign for American preferences. Ended in dealer litigation. Optimism substituted for market research. |

| Two-Wheeler Business | 2008–2020 | Significant | Zero brand equity in urban two-wheelers against Hero, Bajaj, and TVS. Portfolio completeness is not a strategy. Multiple restarts, all failed. Eventually exited clean. |

| Mahindra Reva / EVs Mk1 | 2010–2016 | Strategic | Technology and charging infrastructure not ready. Market was ten years ahead of ecosystem readiness. Early entry does not guarantee durable advantage without the surrounding infrastructure. |

| Sampo / Mitsubishi Agri Machinery | Exited 2021 | Framework Exit | Failed the 18% ROE threshold under Capital Allocation 2.0. Clean, swift exit with clear public rationale — the new framework operating exactly as intended. |

Download the Full Mahindra & Mahindra Case Study

This article is drawn from a 70-plus page case study covering M&M's complete 80-year evolution, the full mechanics of all seven business verticals, the INGLO EV technical architecture, ownership structure analysis, the complete Capital Allocation 2.0 framework, five strategic lessons, the full failed ventures audit, and six material risk scenarios. The PDF is free.

PDF not loading? Open in a new tab.

Mahindra & Mahindra: The Federation That Refused to Die

The complete 80-year business case study. Seven verticals. Six failures. One framework that changed everything. Written for business readers, analysts, and founders.

Download the Free M&M Case StudyPlease rate my work

Your page rank: