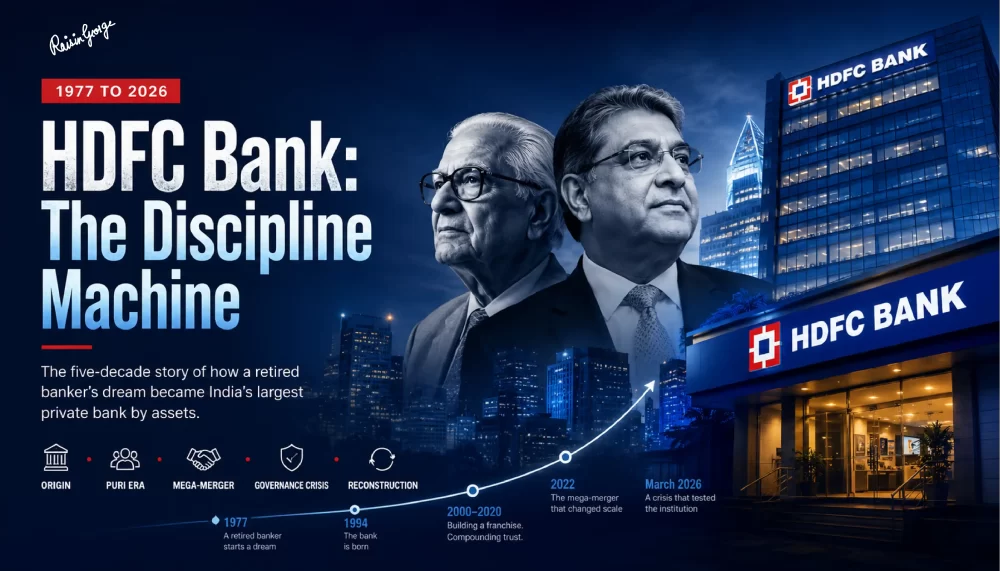

In February 1994, Deepak Parekh made a phone call to a Citibank office in Kuala Lumpur. An eight-year-old girl answered. Her father — Aditya Puri, then CEO of Citibank Malaysia — came to the phone. Within minutes, he had been offered a 50 percent salary cut to come back to India and build a bank from scratch. He accepted. Twenty-six years later, that bank had delivered total shareholder returns of more than 16,000 percent, and The Economist was asking, somewhat seriously, whether Aditya Puri might be the world's best banker.

HDFC Bank is India's largest private bank by assets, with a balance sheet crossing ₹43 lakh crore in March 2026. It is the first and only Indian bank to have maintained Gross NPA below 1.5 percent through an industry-wide crisis in which peers averaged 12–15 percent bad loans. It built the 10-second personal loan before any competitor understood that instant underwriting was possible. It survived a ₹40 billion mega-merger and a chairman's dramatic resignation in the same three-year window. And it did all of this while never once deviating from a principle that its founding CEO said so casually it almost sounds like a joke: "Friendship and banking are not correlated."

This article covers ten things about HDFC Bank that most readers — including most investors — do not know. The complete 70-plus page case study is available at the bottom.

The complete HDFC Bank case study — covering the full Puri era, the CASA flywheel mechanics, the merger deep-dive, the governance episode, all six key risks, and the financial model — is available as a free PDF at the end of this article.

Origin1. India's Largest Private Bank Was Born From a Post-Retirement Project

H.T. Parekh — Hasmukh Thakordas Parekh — was 65 years old when he started HDFC Ltd in 1977. He had just retired as Executive Chairman of ICICI, the institution he had built into India's premier development finance institution. Most men of that profile and era would have taken a governorship, an advisory board seat, or a ceremonial directorship. H.T. Parekh looked at India's housing finance problem — hundreds of millions of people with no access to long-term mortgage credit — and built the institution that eventually became the parent of India's largest private bank.

The environment was structurally hostile. There was no precedent for individual retail mortgage lending at scale. Formal banks did not lend to individuals for housing. Most Indians were, as Deepak Parekh later described them, "extremely debt averse." Foreclosure norms were weak. Title records were chaotic. Black money participation in real estate was large enough to make documentation of property values unreliable.

The funding model that made it work: H.T. Parekh solved the capital problem by borrowing from international development agencies — the IFC (World Bank arm), international insurance companies — at wholesale rates, and deploying those funds as retail home loans to India's emerging middle class. No domestic precedent. No local competition for years. The business model was structurally protected by the novelty of the thing itself. When Deepak Parekh later saw the opportunity to extend the HDFC franchise into banking, the brand equity, nationwide deposit franchise, and retail customer base that H.T. Parekh had built were the foundations everything else was built on. The bank that became worth ₹11 lakh crore was the post-retirement project of a 65-year-old's act of institutional imagination in 1977.

The institution H.T. Parekh built even created competition for itself: GRUH Finance (1986), backed by IFC and the Aga Khan Foundation, specifically to reach Tier II and III towns. His own rationale: "By creating a network of HDFC financial service institutions, we are exporting essentially a style that reflects a carefully developed world view." HDFC Bank, HDFC Life Insurance, HDFC AMC — each a separate expression of the same world view, assembled over four decades from one man's post-retirement clarity of purpose.

Founding Moment2. A CEO's Eight-Year-Old Daughter Answered the Call That Built India's Biggest Private Bank

The founding recruitment of HDFC Bank was not a process. It was a Thursday morning phone call, a salary cut, and a return to a country that was still figuring out what private banking meant.

In February 1994, Deepak Parekh called Citibank House in Kuala Lumpur. When Aditya Puri's daughter Amrita — eight years old at the time — answered the phone, she called her father: "Papa, a Mr Parekh is on the line." Puri came to the phone. Deepak told him: "You run around the world a lot. Now come back to the country, do some real work, build a bank." Puri said he wanted complete management freedom. Deepak agreed: "No, it will be your bank. I won't even be on the board. It will be run by professional management and you will head that."

When Puri asked about the salary, Deepak's response became something of a founding legend: "Arre baba, you have earned enough. Now do something for the nation." Puri accepted a 50 percent salary cut to leave the most prestigious banking platform in Asia and return to India. Amrita Puri went on to become a Bollywood actress. Her father went on to build what The Economist would eventually describe as potentially the world's best-run bank.

The pattern repeats: This recruitment story has a precise structural echo. In 1978, sixteen years earlier, Deepak Parekh himself had taken a 50 percent salary cut to join H.T. Parekh's HDFC Ltd — leaving Chase Manhattan Bank's regional role. In this institution, the founding gesture — taking less money to build something from scratch — was not just biography. It was cultural protocol. The institution was built by people who chose it over comfort, twice.

Puri arrived in India to a first office with broken chairs. The team worked in a rat-infested Mumbai space, drank fizz drinks, wore popular mid-market footwear, and made plans to build a world-class institution. Nobody thought it was possible. The IPO in March 1995, when the bank had exactly one branch and ₹100 crore of capital, was oversubscribed 55 times. The market believed it before the institution existed.

The Puri Era3. The Banker Who Didn't Carry a Mobile Phone Built India's Most Advanced Digital Bank

Aditya Puri ran HDFC Bank for exactly 26 years — from September 1994 to October 2020 — the longest tenure of any CEO at a private Indian bank. He retired at 70. His foundational insight, articulated at the very start and never revised, was surgical: foreign banks had the product and service quality. Public sector banks had the brand, the scale, and the customer base. Nobody had both. "If we can get together a bank that can combine the quality of a foreign bank with the scale and reach of a public-sector bank, with the right technology investments, then it would be a winner." That sentence, and 26 years of relentless execution of it, is the complete HDFC Bank story.

"I speak to you; you don't speak to me. I don't appreciate a call when I've just had my bath, finished my exercise, put on my music and poured my drink of Scotch."

— Aditya Puri, on why he did not carry a mobile phoneThe detail is more revealing than it first appears. The man who championed India's 10-second loan, built the country's most sophisticated retail credit scoring engine, and personally visited Silicon Valley to assess the fintech threat — did not carry a mobile phone. He was not a technologist evangelising digital because it sounded modern. He was a banker who deployed technology precisely and clinically, because it solved specific banking problems. Digital was a tool, not an identity. This distinction — between institutions that embrace technology as strategy and those that embrace it as fashion — matters enormously to the cultural quality of execution.

The succession was as deliberate as the tenure. Puri identified Sashidhar Jagdishan — a colleague since 1996 and CFO since 2008 — as his successor, and eighteen months before the handover gave him a new designation: "change agent." Everyone laughed at the title. The intent was precise: force the identified successor to formally challenge the bank's existing processes before inheriting the chair. Jagdishan's first act as change agent was an instruction to go break things — "come back to me with answers." It is how an institution transmits institutional discipline without transmitting institutional rigidity.

Business Model4. The Salary Account Flywheel — How HDFC Bank Made India's Employers Its Marketing Department

The most important strategic decision in HDFC Bank's history was not a product launch. It was a distribution decision made in the early 2000s: become the default payroll bank for India's organised employment sector. The logic was simple, the execution was relentless, and the competitive consequence compounded for two decades.

When a company signs a payroll agreement with HDFC Bank, every employee gets a salary account — at zero customer acquisition cost. The bank does not spend on advertising, branches, or salespeople to acquire that customer. The employer's HR department does it. What arrives in the bank's hands is a relationship with a documented income earner, beginning on their first payday.

By March 2004, HDFC Bank had over 12,000 companies disbursing payrolls through its system, covering more than 1.1 million salary accounts. By FY24, salary account deposits exceeded ₹1.9 lakh crore — roughly 9 percent of the bank's total deposit base at the time.

Why the moat is structurally durable: Employees rarely switch salary accounts because their EMIs, SIPs, and utility bill payments are linked to them — the friction is operational, not commercial. Employers rarely switch payroll banks because the HR system reconfiguration, staff communication, and IT integration cost is significant. The relationship is doubly sticky: the employee cannot leave easily, and the employer will not switch unless the service deteriorates materially. This is not brand loyalty. It is structural lock-in at scale, built into the fabric of India's organised employment sector.

5. When India's Banking System Collapsed, HDFC Bank's Bad Loans Never Crossed 1.4%

Between 2012 and 2020, India's banking sector accumulated non-performing assets that crossed ₹10 lakh crore. Yes Bank collapsed requiring a ₹25,000 crore emergency rescue. IL&FS defaulted on ₹91,000 crore of debt. Public sector bank gross NPA ratios averaged 12–15 percent during the crisis years. Even ICICI Bank — the other flagship of Indian private banking — spent years managing its own stressed corporate book and lost the market leadership position it had held.

HDFC Bank's GNPA through this entire period: below 1.4 percent.

This was not luck. It was four specific, institutionalised decisions:

| Credit Principle | What It Meant in Practice | Outcome |

|---|---|---|

| No infrastructure lending | While peers chased large project loans with political prestige, HDFC Bank systematically excluded long-tenure, illiquid, politically exposed infrastructure loans from its corporate book | Zero exposure to the ₹10L crore NPA pile that destroyed PSU balance sheets |

| "Friendship and banking are not correlated" | Relationship managers had limited individual authority to override credit decisions. Credit and origination functions were independent. No lending to Vijay Mallya. No lending to Nirav Modi. | Zero exposure to the decade's largest fraud cases |

| Pilot before scale | Every new lending product — personal loans, credit cards — was piloted at small scale, defaults measured honestly, models refined, scale approved only when default rates were validated | Unsecured book grew without NPA accumulation that plagued peers who scaled faster than their models could support |

| Early recognition | When assets showed stress, HDFC Bank provisioned immediately — no "ever-greening," no restructuring to delay recognition. Short-term profit hits. Long-term balance sheet integrity. | Clean balance sheet through every cycle without the "can-kicking" that turned manageable NPAs into existential crises at peers |

The competitive reward was compounding: While ICICI Bank spent years managing its stressed corporate book, HDFC Bank grew. Net advances increased from ₹1.98 lakh crore in FY13 to ₹11.32 lakh crore in FY23 — a 5.7x increase in a decade during which competitors were shrinking their books to survive. HDFC Bank overtook ICICI Bank as India's largest private bank not through aggressive growth, but through disciplined lending while peers were distracted by their own balance sheets. The best competitive move of the decade was simply refusing to make the loans that destroyed everyone else.

6. The Only Bank in India That Appealed Against an RBI Directive — and Was Right

When the Reserve Bank of India directed all banks to make additional provisions against a specific stressed corporate account, every bank complied without formal challenge. One bank appealed through proper channels: HDFC Bank. The credit assessment function had independently evaluated the account and disagreed with the regulator's instruction.

This is not the behaviour of an institution seeking to avoid accountability. This is the behaviour of an institution sufficiently confident in its own credit analysis to challenge a regulator through the correct formal process — not to avoid the outcome, but to seek a review of the basis for the decision.

The account subsequently showed stress. HDFC Bank took the provision immediately, without the extended delay or restructuring that other banks employed. Its formal challenge was overruled but its credit assessment was vindicated in substance: the account was impaired, and HDFC Bank recognised this the moment the stress materialised rather than rolling forward.

What this reveals about institutional culture: A bank with an independent credit function strong enough to formally challenge a regulator's instruction, and honest enough to provision immediately when the credit deteriorates, is structurally different from a bank whose credit function answers to the relationship manager or the quarterly earnings target. The RBI appeal was not a headline event. It was a data point about the quality of HDFC Bank's internal governance at the level that actually determines long-term performance — the credit decision, not the press release.

7. The $40 Billion Merger Was Right. It Was Also Slower Than Planned. Both Things Are True.

In April 2022, HDFC Ltd and HDFC Bank announced a merger valued at approximately $40 billion — one of the largest financial mergers in Asian corporate history. The strategic logic was compelling on paper and remains sound in principle. The execution produced three years of painful metric compression that the market has only partially digested.

Merger announced. Shareholders to receive 42 HDFC Bank shares per 25 HDFC Ltd shares. Strategic rationale: HDFC Ltd's ₹7L crore+ mortgage portfolio funded through HDFC Bank's low-cost CASA deposits, unlocking 150–200 bps margin improvement.

Merger effective. CD ratio crosses 110% (target: 85–90%). CASA ratio falls from 44% to ~37–38% immediately. NIM compresses from ~4.3% to ~3.3%. The problem is structural: HDFC Ltd's funding was wholesale bonds, not CASA deposits. The balance sheet merged; the liabilities did not instantly convert.

CEO Jagdishan makes an extraordinary public commitment: deliberately slow loan growth to 5.4% (well below system) to allow deposit growth to catch up. ₹46,300 crore of loans securitised. Deposit growth 14%. CD ratio pulled from 110%+ toward 100%.

Balance sheet: ₹43.6 lakh crore. Net profit: ₹19,221 crore (+9.1% YoY). GNPA: 1.15% (ex-agri: 0.91%). CD ratio: ~95–96%. Loan growth recovered to 12%. Trajectory: correct. Timeline: longer than management originally guided.

Why the thesis remains intact: Post-merger, 80 percent of new HDFC home loans went to customers who already held an HDFC Bank savings account — demonstrating the cross-sell benefit immediately. The India-wide network now sells home loans, credit cards, insurance, and investment products to the same customer. The mortgage book's lower yield (8.5–9%) vs. credit cards and personal loans (14–18%) structurally compresses margins — but this is a known, finite transition problem, not a permanent structural impairment. Management's FY27 guidance: loan growth outpacing the system for the first time since the merger. The destination is intact. The timetable was optimistic.

8. The 10-Second Loan Was Not a Technology Innovation. It Was a Data Innovation.

When HDFC Bank launched the 10-second personal loan — pre-approved disbursals to existing customers' accounts in under ten seconds, entirely through digital channels, with no human underwriting — the industry framing was "fintech-style innovation." The framing was wrong. The technology was a disbursement API. What made the product possible was twenty years of data.

An HDFC Bank salary account holder, by the time the 10-second loan was offered to them, had already given the bank complete information: documented monthly income (salary credits visible for years), existing EMI obligations (debiting through the same account), spending patterns (UPI and card transactions), and credit behaviour (whether prior loan payments were made on time). The underwriting was complete before the customer clicked "apply." The ten seconds was the time required to execute a decision that had, in effect, already been made.

"Nobody could do it then — and many still can't." That quote, from Puri in 2020, was accurate. Banks with fragmented customer data, legacy core banking systems, and limited relationship history could not replicate the product regardless of their technology investment. A fintech startup with a polished app and modern infrastructure but no pre-existing relationship with the customer faces the same problem: the underwriting still requires data collection, verification, and processing. HDFC Bank's data came pre-built, pre-verified, and pre-structured through the salary account relationship. The app was the interface. The 20-year relationship was the product.

Puri went to Silicon Valley in the mid-2010s when the disruption narrative was loudest, specifically because he needed to understand what fintech companies were building. His conclusion: they had beautiful interfaces but lacked brand, distribution, and trust. He came back and said the bank was not going to be disrupted — it was going to be the disruptor. The 10-second loan was the proof point. 97 percent of HDFC Bank's active clients use digital platforms today. The bank that the fintech industry thought was a dinosaur became India's largest technology deployer in retail banking, spending approximately $1 billion annually on technology and running 5 AI use cases in production as of FY26.

Governance Episode9. The Chairman's Resignation That Wiped ₹1 Lakh Crore — and Was Quietly Resolved

On the night of 18 March 2026, HDFC Bank filed a late exchange notification: Atanu Chakraborty, the bank's part-time non-executive Chairman, had resigned with immediate effect. His resignation letter stated that "certain practices within the bank over the past two years were not in alignment with personal values and ethics."

The market did not wait for context. HDFC Bank shares fell 9 percent intraday on 19 March. Market capitalisation declined by over ₹1 lakh crore within a week. American Depositary Receipts fell 8 percent.

Chakraborty resigns with immediate effect, citing ethical misalignment. A 1985-batch IAS officer, retired Secretary of the DEA, the most powerful bureaucratic position in India's finance ministry — resigned with 14 months left on his RBI-approved term.

Shares fall 9% intraday, ₹1L crore market cap wiped. RBI makes an unusually direct statement: "HDFC Bank is a D-SIB with sound financials, professionally run board, and competent management team. Based on our periodical assessment, there are no material concerns on record as regards its conduct or governance." Keki Mistry — former VC and CEO of HDFC Ltd — appointed interim Chairman.

Two Mumbai law firms — Trilegal and Wadia Ghandy & Co — commissioned to review board minutes and video recordings of meetings over three years. Proxy advisor InGovern characterises resignation as "likely driven by individual personality differences rather than any threat to shareholder value."

Law firm review finds no major governance lapses. CEO Sashidhar Jagdishan's reappointment — which had been in formal uncertainty — cleared. Board asks Chakraborty to reconsider, fails. Mistry confirmed as interim chairman. Resolution: quiet. Market: partially recovered.

What the episode actually showed: A single governance event — ultimately found by independent legal review to involve no major lapses — erased more market value in a week than many Indian companies have ever created in total. This is the fragility of trust when trust is the primary asset. HDFC Bank's entire valuation premium over peers rests on the presumption of institutional integrity. When that presumption was placed in doubt, even briefly and without factual basis, the market repriced ₹1 lakh crore of value in hours. The lesson is not about the specific events of March 2026. It is about what happens to trust-dependent institutions when trust is even momentarily questioned — regardless of underlying facts.

10. HDB Financial Services: The High-Yield Bank-Within-a-Bank Most Analysts Overlook

HDFC Bank's majority-owned subsidiary HDB Financial Services is, in effect, a mid-size Indian bank operating at margins the parent can no longer achieve post-merger. As of Q4 FY26: NIM of 8.2 percent, Return on Assets of 2.5 percent, Return on Equity of 14.8 percent. Compare these to HDFC Bank's own NIM of 3.38 percent and ROA of approximately 1.96 percent.

HDB Financial serves 22.9 million customers across 1,730 branches in 1,161 cities — scale comparable to a mid-size Indian bank. Its customer base occupies the credit segment just below HDFC Bank's threshold: borrowers who are creditworthy but do not meet the parent bank's income or documentation standards. HDB charges higher rates (reflecting higher risk), generates higher margins, and posted Q4 FY26 net profit growth of 41 percent year-on-year.

The subsidiary completed its IPO in FY26, creating public market visibility and an independent valuation. The strategic architecture is elegant: HDFC Bank serves the prime customer with low-margin, high-volume banking. HDB Financial serves the near-prime customer with high-margin, growth-stage lending. Together they cover the full creditworthy Indian population without either entity compromising its risk profile for the sake of volume.

Why most analysts underweight it: HDB Financial does not appear in HDFC Bank's standalone financials — it is a consolidated subsidiary. Analysts focused on NIM, CASA ratio, and CD ratio at the consolidated level often treat HDB as a rounding error. It is not. At 2.5% ROA, 14.8% ROE, 8.2% NIM, and 41% profit growth, HDB Financial Services is the highest-returning business in the HDFC Bank group — and it is expanding faster than the parent.

Ten Facts About HDFC Bank That Rarely Appear in Analyst Reports

H.T. Parekh started HDFC Ltd at age 65, after retiring as ICICI's Executive Chairman. The institution that became India's largest private bank was the post-retirement project of a man most organisations would have considered past his productive years.

When Deepak Parekh called Citibank Malaysia to recruit Aditya Puri, Puri's eight-year-old daughter Amrita answered the phone. She went on to become a Bollywood actress. Her father took the call, accepted a 50% salary cut, and spent 26 years building India's largest private bank.

When banking licences were opened in 1993, Deepak Parekh proposed applying. The HDFC board said no. His influence eventually carried the room. HDFC Bank exists because one man was persuasive enough to overcome his own board's institutional resistance.

HDFC Bank's February 2000 merger with Times Bank was the first-ever private-sector bank merger in India — a structure with no domestic precedent. HDFC Bank established the template for what would become a widespread consolidation mechanism in Indian banking.

The instant personal loan had no machine learning breakthrough at its core. It had two decades of salary credits, EMI payments, and spending patterns on a specific customer, combined with a disbursement API. The technology took months to build. The data took twenty years.

When the RBI directed all banks to provision against a specific corporate account, HDFC Bank was the only institution that formally appealed through proper channels. The credit function disagreed with the regulator. It challenged institutionally, provisioned immediately when stress materialised, and was vindicated in substance.

Aditya Puri — who championed AI underwriting, instant digital loans, and India's most advanced retail banking platform — famously did not carry a mobile phone. He was not a technologist evangelising digital. He was a banker deploying technology precisely, as a tool.

By FY24, HDFC Bank's salary account deposits alone exceeded ₹1.9 lakh crore — roughly 9% of the total deposit base at the time. The entire sum arrived at near-zero cost, generated by the employer, delivered without a single rupee of advertising spend.

The March 2026 chairman's resignation wiped ₹1 lakh crore of market cap in a week. Independent law firms subsequently reviewed three years of board minutes and video recordings. Finding: no major governance lapses. The cost of trust, when it is briefly questioned, is ₹1 lakh crore — regardless of the facts.

The founding promoter group holds approximately 5–8% post-merger. Foreign Portfolio Investors hold ~34–36%; domestic institutions ~26–28%. HDFC Bank is institutionally owned and institutionally accountable in a way that no family-controlled Indian conglomerate can claim. Capital Allocation is forced to make sense — publicly, quarterly, forever.

The Six Material Risks — Plainly Stated

| Risk | Severity | What It Actually Means |

|---|---|---|

| NIM Recovery Problem | Medium | The large, lower-yield mortgage book structurally compresses margins. Recovery to pre-merger NIM requires either repricing mortgages (losing customers to competitors) or growing high-yield unsecured faster (risking NPA rise in slowdown). No easy path. |

| CASA Restoration Challenge | Medium | Restoring CASA from ~38% to ~44% is organic and slow — it requires deepening relationships, not offering higher rates. In an environment where peers aggressively price time deposits to attract savers, organic CASA growth is harder than it looks. |

| CD Ratio Overhang | Medium | FY27 guidance of loan growth outpacing the system while further reducing the CD ratio is arithmetically demanding. Requires exceptional deposit mobilisation or slower-than-guided loan growth — the same trade-off the bank has navigated since July 2023. |

| Technology / Data Portability | Structural | India's Account Aggregator framework allows customers to share HDFC Bank transaction data with other lenders. The competitive moat built on proprietary data is partially exposed to regulatory portability norms being incrementally expanded. |

| RBI Regulatory Risk | Medium | HDFC Bank has accumulated multiple regulatory interactions: IT outage-related credit card ban (2020), AT-1 bond mis-selling at DIFC branch (2026), governance episode (2026). As a D-SIB, its regulatory relationship is structurally closer and more consequential than for smaller peers. |

| Leadership Continuity | Watch | 26 years of compound performance under one CEO created an institutional culture that is now being transmitted through a second transition. The March 2026 episode demonstrated that leadership continuity — one of HDFC Bank's structural advantages — cannot be taken for granted. No process documentation fully substitutes for cultural transmission. |

Download the Full HDFC Bank Case Study

This article draws from a 70-plus page case study covering the full Aditya Puri era in detail, the mechanics of the salary account flywheel, the complete CASA and NIM financial model, the HDFC Ltd merger deep-dive, the governance episode timeline, all six material risks, five strategic lessons, a complete historical timeline from 1977 to May 2026, and the full sources and legal disclaimer. The PDF is free.

PDF not loading? Open in a new tab →

HDFC Bank: The Discipline Machine

The complete case study. 1977 to 2026. The Puri era, the salary account flywheel, the NPA miracle, the $40B merger, and the governance drama that erased ₹1 lakh crore overnight. Written for business readers, analysts, and founders.

Download the Free HDFC Bank Case Study →Please rate my work

Your page rank: