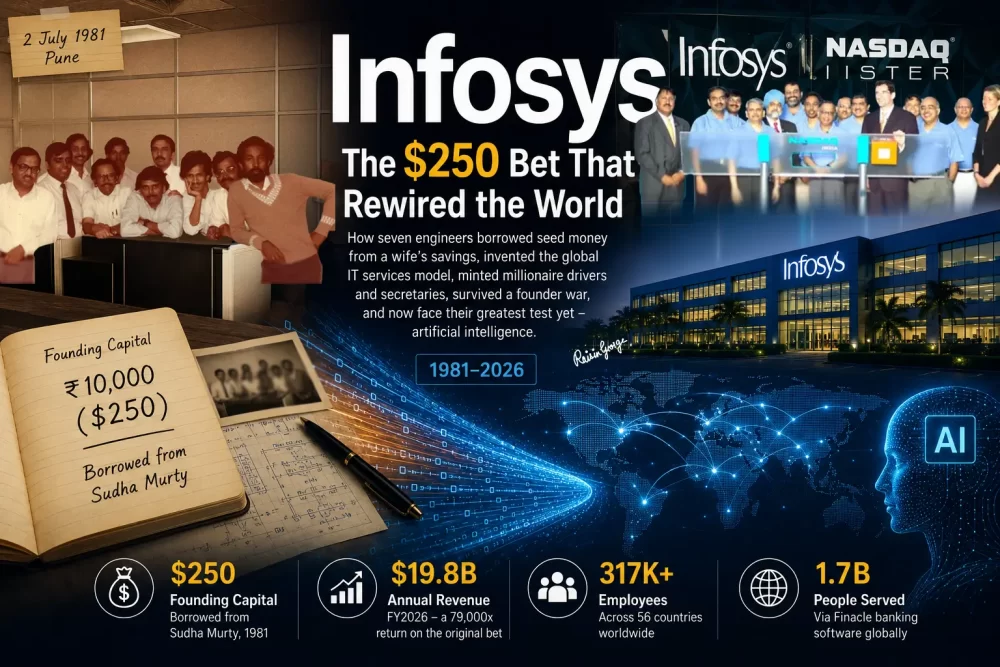

In July 1981, seven engineers pooled together ₹10,000 — approximately $250 at the time, borrowed by Narayana Murthy from his wife Sudha. There was no office. No computer. Their first client was in New York. Their first product was a payroll package delivered on a borrowed machine.

Forty-five years later, Infosys employs over 317,000 people across 56 countries, earns $19.8 billion in annual revenue, powers the core banking systems of 1.7 billion people worldwide through Finacle, and sits at the centre of one of the most consequential debates in the history of the software industry: what happens to the world's largest IT services firm when artificial intelligence begins doing what IT services firms do?

This is not a story about a company that got lucky. It is a story about a business model invented from first principles, replicated by every competitor, exported across the world — and now being renegotiated by the very technology it helped deploy.

Origin Story

Hook 1: $250, a Borrowed Dream, and No Computer

The story of Infosys begins not with venture capital, not with a university lab, and not with a government contract. It begins with a kitchen-table decision made by seven engineers who were, by any reasonable measure, taking a catastrophic risk.

Narayana Murthy, Nandan Nilekani, S. Gopalakrishnan, S.D. Shibulal, K. Dinesh, N.S. Raghavan, and Ashok Arora had all been colleagues at Patni Computer Systems in Pune. They resigned together in 1981 and incorporated Infosys Consultants Private Limited — the name chosen not for strategy, but because it was available.

The ₹10,000 (~$250) in founding capital came from Murthy's wife, Sudha Murty, who would go on to become one of India's most beloved philanthropists, authors, and Rajya Sabha members. The founding team operated from Murthy's apartment in Pune. They had no computer of their own — for nearly two years, they developed software on client machines.

The detail most people miss: Importing a single computer in 1981 required a government licence under India's License Raj — a process that could take close to a year. Infosys was not a slow-moving startup. It was a company being strangled by bureaucracy before it had revenue. The founders flew economy, stayed in budget hotels, and sometimes walked instead of taking cabs. Every rupee was tracked.

Their first client, Data Basics Corporation in New York, commissioned a payroll package. Murthy managed the US relationship while his co-founders built in India — a prototype of the onsite-offshore model that would later become the Global Delivery Model and transform the global IT industry.

Founder Philosophy

Hook 2: The Communist Prison That Made a Capitalist

Before Infosys, Narayana Murthy was a committed socialist. He had studied in France, been influenced by left-wing student movements of the 1960s, and believed collective economic models held the answer to poverty.

That belief was broken — literally — during a train journey through Eastern Europe in the 1970s. Murthy was travelling through Bulgaria when authorities detained him at a rail station, held him overnight, and confiscated the food his friend had packed for the journey.

The Bulgaria moment is not a footnote. It is the source code of Infosys's entire operating philosophy: capitalism, yes — but capitalism practised ethically, transparently, and with explicit obligations to employees, customers, investors, and society. Every decision Murthy made at Infosys — from the ESOP structure to the governance disclosures to the voluntary adoption of US GAAP — traces back to this conversion.

Business Model Invention

Hook 3: The Model Every Company in the World Now Copies

Infosys did not invent software. It did not invent outsourcing. What it invented — in the mid-1990s, in the years immediately after India's 1991 liberalisation — was a delivery architecture for software that had never existed at scale before. That architecture is called the Global Delivery Model, and it is now the operational standard for every IT services firm on earth.

The genius of the GDM was not cost savings — though that was the headline benefit for clients. The deeper genius was the 24-hour development cycle: a client in New York hands off requirements at 6 PM; India's team picks them up at 7:30 AM. By the time the New York client arrives the following morning, a day's work has been completed overnight. Software development, conceptually, never sleeps.

After Infosys formalised and scaled the GDM in the mid-1990s, revenues grew fourfold in four years. TCS, Wipro, HCL, Accenture GBS, IBM Global Services, Capgemini — every firm in the global IT services industry now operates a version of the model Infosys built.

Wealth Creation

Hook 4: The ESOP That Made Drivers and Secretaries into Millionaires

In 1994, three years after India's liberalisation and a year after its IPO, Infosys introduced what would become one of the most consequential employee benefit programmes in Indian corporate history: a formal Employee Stock Option Plan, or ESOP.

This was not unusual by global standards. US technology companies had been granting stock options for years. What made Infosys's ESOP extraordinary was its breadth. Every employee — including drivers, office assistants, and secretaries — received shares at a deep discount to market price.

What happened next: After the 1993 IPO and subsequent price appreciation, hundreds of Infosys employees became dollar millionaires. Thousands became rupee millionaires. Administrative staff who had accepted positions at modest salaries found themselves holding wealth that transformed their families' trajectories. Murthy later said: "Today, every Indian employee at every level who joined us on or before March 2010 is a stockholder of Infosys." Total ESOPs distributed since inception: worth over ₹50,000 crore.

The ESOP democratised wealth in a country where corporate ownership had historically been the exclusive domain of founding families and institutional investors. What Infosys did was distribute equity to the people who answered the phones, drove the cars, and made the chai. That decision set a precedent — and made Infosys the most aspirational IT employer in India for over a decade.

Global Capital Markets

Hook 5: The NASDAQ Bell Rung From Mysore

On March 11, 1999, Infosys Technologies became the first Indian company to list on the NASDAQ Stock Market. Ticker: INFY.

The moment was staged with deliberate symbolism. Rather than have Murthy ring the opening bell from New York, Infosys set up the ceremony at its Mysore campus. Three thousand employees gathered on the grounds. Murthy pressed a button. Half a world away on Wall Street, trading began on the NASDAQ National Market.

Why it mattered beyond the listing: To list on NASDAQ in 1999, Infosys had to meet US GAAP accounting standards and SEC disclosure requirements that no Indian company had attempted. The fact that Infosys could do this — voluntarily, before it was required — proved to global capital markets that Indian IT companies were institutionally serious. It opened the door for every subsequent Indian tech listing in the US.

The listing also made Murthy, Nilekani, and the other co-founders dollar billionaires on paper. More significantly, it gave Infosys the global capital needed to fund the Mysore campus, the expansion of international delivery centres, and the formalisation of the GDM at scale.

Corporate Governance

Hook 6: The Governance Framework That India Built Its Rules Around

In the late 1990s, Indian corporate governance was largely a private affair. Boards were dominated by promoters. Audit committees were nominal. Disclosure was minimal. Most companies did little more than the Companies Act required.

Infosys chose a different path — not because it was forced to, but because Murthy believed transparency was itself a competitive advantage.

What Infosys did that no Indian company had done: Published India's first corporate governance compliance report (based on CII recommendations). Adopted US GAAP voluntarily — years before SEBI required convergence. Established fully independent audit, compensation, and risk committees. Adopted the operating principle: "When in doubt, disclose." Committed to satisfying the spirit of the law, not just the letter.

SEBI's subsequent corporate governance regulations — introduced through Clause 49 of the Listing Agreement and later the Companies Act 2013 — were substantially modelled on the standards Infosys had voluntarily adopted a decade earlier. NASSCOM governance frameworks for Indian IT companies benchmarked against Infosys. The company did not just build a business. It built the institutional template the Indian corporate sector later adopted under regulatory compulsion.

Institutional Scale

Hook 7: The World's Largest Corporate University — Spelled From Space

In 2005, Infosys inaugurated its Global Education Centre (GEC) in Mysore — a 337-acre campus that functions as the world's largest corporate training facility. The GEC can accommodate over 14,000 employees simultaneously. It runs a 23-week residential programme for all new engineering hires, graduating approximately 20,000 employees annually.

The fact that stops every conversation: The buildings of the Mysore campus, when viewed on Google Maps from satellite, are arranged so that their layout spells the word "INFOSYS." A deliberate architectural decision. Visible from space.

Hidden Empire

Hook 8: Finacle — The Banking Software Nobody Talks About

Most people think of Infosys as a pure IT services company — a firm that deploys engineers to build and maintain software for other people's businesses. That description is correct, and accounts for roughly 85% of Infosys's revenue. What it misses is Finacle.

Launched in 1999 and now operated through EdgeVerve Systems (a wholly-owned Infosys subsidiary), Finacle is a core banking software platform used by banks in over 100 countries, serving more than 1.7 billion people. The client list reads like a directory of the world's most important financial institutions: State Bank of India, ICICI Bank, Punjab National Bank, HDFC Bank, Bank of America, RBC Wealth Management.

A pure IT services company quietly building a product that runs global banking infrastructure — that is Finacle. It competes directly with Temenos, Oracle FLEXCUBE, TCS BaNCS, and FIS. And it does so from a company that most analysts evaluate purely as a headcount-and-billing model.

Corporate Drama

Hook 9: The Founder Who Came Back to Destroy the CEO He Endorsed

In 2014, Infosys made a historic appointment: Vishal Sikka, former CTO of SAP and a Stanford PhD in artificial intelligence, became the first non-founder CEO in Infosys's history. The board celebrated. The market celebrated. Sikka brought ambition, Silicon Valley energy, and a vision for AI-led transformation that Infosys had visibly lacked.

Under Sikka, revenues grew approximately 25% over three years. He launched the Zero Distance programme — requiring every project team to bring innovation to every client engagement. The stock rose 21%.

Then Narayana Murthy began writing letters.

The governance paradox: The founders who built Infosys on a philosophy of transparent governance were themselves responsible for one of the most damaging acts of governance aggression in Indian corporate history. Murthy held only ~3–4% of shares — yet his institutional authority was sufficient to bring down a CEO who had delivered growth. The lesson: in a company built on the founder's moral reputation, the founder never fully leaves.

Existential Reckoning

Hook 10: The AI Paradox — Threatened, Positioned, and Racing Against Time

The question hanging over every large IT services company in 2026 is the same: if artificial intelligence can write, test, debug, and maintain software — what exactly is a 317,000-person IT services firm for?

Infosys is the most interesting case study in how to answer that question — because it is both the most threatened and the most active responder.

Clients need fewer engineers to do the same work.

The headcount-billing model breaks if productivity per engineer doubles.

Discretionary IT budgets already frozen in 2023–24.

Topaz AI platform — proprietary GenAI toolkit for clients.

Partnerships: Anthropic, OpenAI, NVIDIA, Google, Microsoft, AWS.

6 AI value pools identified — TAM: $300B+.

AI services: 5.5% of revenue in Q3 FY26, growing fast.

Leadership

The CEO Relay Race: Seven Leaders, One Company

Financials

The Numbers: FY2022 to FY2027 Guidance

| Metric | FY2022 | FY2023 | FY2024 | FY2025 | FY2026 est. | FY2027 Guidance |

|---|---|---|---|---|---|---|

| Revenue (USD) | $16.3B | $18.2B | $18.6B | $19.1B | ~$19.8B | 1.5–3.5% CC growth |

| Revenue Growth (CC) | +19.7% | +15.4% | +1.4% | +4.2% | +3–3.5% | Guided acceleration |

| Operating Margin | 22.7% | 21.0% | 20.7% | 21.1% | ~21% | Stable |

| Net Profit | ~$2.9B | ~$3.1B | ~$3.2B | ~$3.4B | ~$3.5B | Growing |

| Large Deal TCV | — | $9.8B | $17.7B (record) | $11.5B | $12B+ | 80% net new in FY26 |

| Headcount | 314,000 | 343,000 | 317,000 | 323,000 | ~315,000 | AI productivity impact |

| Attrition | 27.1% (peak) | 20.9% | 12.9% | 13.7% | Stabilising | — |

| Market Cap | ~$90B | ~$65B | ~$75B | ~$80B | ~$90–95B | — |

The growth paradox in the numbers: FY2022 saw 19.7% growth — a COVID-era surge in digital transformation spending. FY2024 saw only 1.4% — macro-driven freeze. FY2025 recovered to 4.2% on large deal ramp-ups. The pattern reveals that Infosys's revenue is highly correlated with global enterprise discretionary IT spending — making it simultaneously one of India's most globally integrated and most macro-sensitive companies.

The Full Arc

The Ups and Downs: 45 Years of the Roller Coaster

| Year | Event | What Happened & Why It Matters |

|---|---|---|

| ▲ 1981 | Founding | Seven engineers leave Patni. $250 borrowed from Sudha Murty. Company incorporated from Murthy's apartment in Pune. |

| ▼ 1989 | Near-shutdown | US JV partner exits, taking key client with them. All founders consider closing. Murthy pays salaries from personal funds. Survived by the thinnest margin. |

| ▲ 1991 | Liberalisation | India's economic reforms remove the License Raj shackles. Computer imports freed, foreign travel simplified. Infosys growth accelerates immediately. |

| ▲ 1993–94 | IPO + ESOP | Listed on BSE/NSE. Introduced India's first formal ESOP. Drivers and secretaries receive shares. Post-IPO appreciation creates hundreds of millionaires. |

| ▲ 1999 | NASDAQ listing | First Indian company on NASDAQ. Bell rung from Mysore. Opens global capital markets to Indian IT permanently. |

| ▼ 2001–02 | Dot-com bust | US tech clients slash discretionary spending. Revenue growth slows sharply. Murthy steps down as CEO; Nilekani takes over. |

| ▲ 2004 | $1 Billion revenue | Crosses the billion-dollar threshold — positioning Infosys as a global-tier company, not just an Indian IT firm. |

| ▼ 2008–09 | Financial crisis | BFSI sector — Infosys's largest vertical — freezes all IT spending. Revenue growth plummets. Managed without layoffs, but margins compressed. |

| ▼ 2011–14 | Shibulal era drift | Strategy confusion. Infosys loses market share to TCS and Cognizant. First real crisis of strategic identity since founding. |

| ▲ 2014–17 | Sikka growth era | First outsider CEO delivers 25% revenue growth in three years. AI-first vision. Zero Distance programme. Stock rises 21%. |

| ▼ Aug 2017 | Founder-board war | Murthy's campaign forces Sikka's resignation. ₹22,500 crore of market cap destroyed in a single session. Deepest governance crisis in Infosys history. |

| ▲ 2018–24 | Parekh turnaround | Large deal focus. FY2024: record $17.7B TCV. Topaz AI platform. Attrition falls 27% → 12.9%. Revenue crosses $19B. |

| ▼ 2022–23 | Attrition + macro | Post-COVID talent wars push attrition to 27.1%. Salary inflation erodes margins. FY2024 CC growth: only 1.4%. |

| ▲ 2025–26 | AI repositioning | Topaz deployed at scale. 30,000 developers on GitHub Copilot. AI services 5.5% of revenue and growing. Guidance raised mid-FY2026. Record 80% net-new large deal TCV. |

Risks

What Could Go Wrong

| Risk | Severity | Analysis |

|---|---|---|

| AI disrupts the headcount model | High | If AI reduces engineer requirements by 30–40%, the pyramid economics and revenue-per-head model that underpin Infosys's profitability are fundamentally challenged. |

| US visa & immigration policy | High | ~61% of revenue from North America. H-1B restrictions force more local hiring at 3–4× the offshore rate — directly compressing margins. |

| BFSI client concentration | Medium | Financial services is 31% of revenue. A US or European banking crisis triggers the fastest, deepest IT spending freezes. |

| Macro discretionary freeze | Medium | FY2024's 1.4% growth showed how fast clients pause non-essential IT spend. Tariff fears in 2025 triggered another round of client caution. |

| Talent attrition & wage inflation | Medium | The FY22 attrition peak of 27.1% required aggressive counter-offers and mid-cycle salary revisions that compressed margins sharply. Repeatable in a hot talent market. |

| Founder governance activism | Medium | History has demonstrated founders can destabilise management with minority holdings. Institutional memory of 2017 remains strong. Not hypothetical. |

| INR/USD currency risk | Low | Revenue in USD, costs in INR. Rupee appreciation compresses dollar revenue margins. Partially hedged but structurally exposed. |

Lesser-Known Facts

10 Things Most People Don't Know About Infosys

Strategic Lessons

Five Things Infosys Teaches Every Business Builder

Lesson 1: The model matters more than the product. Infosys didn't invent software. It invented the delivery model for software — and that model is now the global industry standard. Competitive advantage can live in the architecture of how you work, not only in what you make.

Lesson 2: Ethics as competitive advantage. Murthy's governance obsession was not a constraint — it was a differentiator. SEBI modelled its governance regulations on Infosys's voluntary standards. That credibility attracted institutional capital at a time when India was not a trusted investment destination.

Lesson 3: ESOP as culture architecture. Distributing equity to drivers and secretaries was not charity. It created a workforce that behaved like owners and made Infosys the most aspirational IT employer in India for over a decade. Incentive alignment is a strategy, not a benefit.

Lesson 4: Founder gravity is both asset and liability. Murthy built Infosys on moral authority. His inability to fully transfer control nearly broke it. Every founder should study the Sikka episode as a governance case — not a personality story.

Lesson 5: The incumbents' dilemma is real — but so is the opportunity. AI threatens Infosys's business model structurally. Its response — partnering with AI companies, deploying Topaz, retraining 30,000 developers, building outcome-based billing — is directionally correct. Whether execution matches ambition is the only question that matters now.

Full Case Study

Read the Complete Infosys Case Study

The complete case study — 1981 to 2026 — is available as a free PDF. Covers the founding story, the Global Delivery Model invention, the ESOP revolution, the NASDAQ listing, the full CEO succession chain, the 2017 founder-board war, Finacle, the AI pivot, detailed financials, risks, and strategic lessons.

PDF not loading? Open in a new tab →

Infosys: The $250 Bet That Rewired the World

The complete case study. 1981 to 2026. Seven engineers, $250, and a borrowed dream — to a $19.8 billion company that invented the model the entire world's IT industry runs on. And now facing its greatest test: artificial intelligence.

Download the Free Infosys Case Study →Please rate my work

Your page rank: